Conclusions

The standard view

An alternative view of hyperinflations

Historical Examples

Conclusions

Weimar Republic Hyperinflation (1922-23)

We’ll start with the most commonly cited example, the Weimar Republic. Germany’s productive capacity had been significantly damaged by World War I, both in terms of the losses inflicted and the resources redirected to military use. Allied troops occupied the Ruhr Valley – the seat of much of Germany’s manufacturing base. These events clearly constituted a large supply shock.

The Republic faced very large foreign claims from war reparations,(13) which had to be repaid in gold. Germany was supposed to export to earn the gold needed to make the payments, but with productive capacity not even capable of meeting domestic demand, there was no chance of exports coming to the rescue.

In 1927, Karl Helfferich (a senior banker at Deutsche Bank) argued that the reparations were to blame for the hyperinflation. He noted that the unfavourable trade balance (lots of imports but no exports) led to depreciation of the currency: “The depreciation of the mark was the beginning of this chain of cause and effect; inflation is not the cause of the increase in prices and of the depreciation of the mark; but depreciation of the mark is the cause of the increase in prices and of the paper mark issues.”(14)

As noted above, Robinson outlined the transmission mechanism, which allowed hyperinflation to rage.

Hungarian Hyperinflation (1945-46)

It appears as if nothing was learnt from the experience of the Weimar Republic as the Hungarian hyperinflation following the end of World War II followed almost exactly the same dynamics. Interesting from my perspective, Hungary poses a real challenge for the quantity theory approach because, for at least a couple of months of its hyperinflation, the authorities literally could not print currency: the retreating fascists had stolen the currency printing plates!

War was once again the terrible supply shock that was visited upon Hungary. Some estimates suggest that as much as 50% of Hungary’s capital stock was destroyed (and some 90% damaged) due to Hungary’s role as a battlefield. Reparations again played their part. Hungary faced requirements to pay financial reparations as well as payments in goods to the occupying Soviet army.

The transmission mechanism seems to have involved a decision by the Hungarian authorities to accommodate the inflationary surge. As Grossman and Horvath pointed out, quoting a member of parliament in 1946, “This inflation . . . could only be barred by methods that would have made it impossible to design a realistic governmental budget.” The authorities believed that their only feasible or viable path was to accommodate the inflation.

In a bid to stabilize tax revenues, the government launched a separate currency for the collection of taxes – the tax pengo. This led to index deposit accounts, and created a situation where all tax payments and pretty much everything else were indexed to the inflation rate.

Chinese Hyperinflation (1937-49)

War (both international and civil) once again played a part in this particular hyperinflation as Japan invaded China in 1937. The Japanese army occupied more than one-third of China and, as a result, important tax revenues from the eastern cities were lost to the Japanese. When the conflict finally ended, it was replaced with a civil war. These terrible events clearly provided a massive and prolonged supply shock to the economy.

Between 1937 and 1949, three governments – the Nationalists, the Japanese, and the Communists – occupied China. Each one issued its own currency (indeed, multiple currencies were issued by each authority). These bodies effectively engaged in monetary warfare, with each producing “propaganda stating that the currency of their enemies was falling rapidly in value.”(15) Depreciation of the various currencies was just a fact of life. This lack of faith created a vicious feedback cycle common in hyperinflations as people held onto the currencies for as little time as possible.

The transmission mechanism was yet again a form of indexation. As people became accustomed to living in high inflation, their wages rose “as fast as prices and even discounted anticipated inflation.”(16)

Botched attempts at stabilization actually exacerbated the supply shock. As Campbell and Tullock wrote, “Imagine the plight of business firms that had borrowed at rates of 1 or 2 per cent per day when the government decided to stop printing more money. A scramble for currency followed, borrowers were unable to pay their debts, and bankruptcies flourished.”

Bolivian Hyperinflation (1984-85)

The roots of the Bolivian experience with hyperinflation can be traced to its near monoculture export base and its heavy reliance on external finance. The former feature meant that when mineral prices fell in the early 1980s (especially tin prices) it had a very serious impact upon GDP and inflation – effectively a classic supply shock.

Bolivia also struggled with heavy external borrowing. Between 1973 and 1981, public long-term external debt rose from $640 million to $2.7 billion. This, of course, left the country vulnerable to any “capital stops.” In the wake of the Mexican default in 1982, such a capital stop occurred.

Add into this mix a newly democratically elected government and the scene was set for disaster. In an effort to dedollarise (17) the economy, President Hernán Siles Zuazo ordered the conversion of all domestic dollar-denominated contracts into peso terms. This unfortunately created yet another run on the peso. The Bolivian authorities also attempted to honour the external debt, creating domestic unrest.

The familiar transmission mechanism of indexation was once again present. One of Zuazo’s policies was to 100% index the minimum wage, with adjustments made with each 40% increase in the price level. This set the standard for other workers who demanded similar treatment. By 1984, there was a policy of 100% indexation for all wages, with a four-month adjustment period. This eventually shrank to just one month. The classic wage-price spiral resulted.

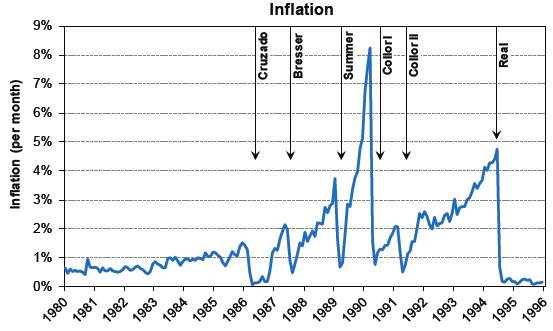

Brazilian Hyperinflation (1987-94)

As with Bolivia, Brazil was subject to the same supply shocks (both physical [oil] and capital related [external debt financing]) in the early 1980s. However, Brazil managed to postpone the arrival of outright hyperinflation longer than many of its neighbours at the cost of very high inflation for a prolonged period (see Exhibit 1).

Exhibit 1

Hyperinflation can only be deferred so long (Brazilian CPI % pm)

Several elements seemed to account for the postponement of outright hyperinflation (and the high inertial inflation). One was widespread indexation. This practice is often part of the wage-price spiral that characterizes hyperinflation. However, in Brazil’s case it predated the hyperinflation and was a well-established practice that gave inflation a strong inertial component.

As Bresser-Pereira and Nakano note, “Inertial inflation tends to be rigid downwards, since future inflation is strongly linked to past inflation. But it also tends to hinder the acceleration of inflation, as long as it avoids or postpones the dollarisation of the economy . . . In Brazil economic agents could protect their financial assets by buying index bonds . . . to buy dollars was risky, first because the parallel exchange rate tended to be artificially high, and second because it would fluctuate markedly.”

As the exhibit highlights, another component of delayed hyperinflation was the various stabilization attempts made by the authorities (five before the Real Plan). Each of these, though ultimately failing, helped reduce inflation on a temporary basis (often due to price freezes). However, each of these plans inflicted a set of costs upon the economy, which cumulatively took their toll (witness the very high levels of capital flight that Brazil suffered) as everyone got used to the “tricks” deployed. The effect was that the failure of each plan resulted in higher and higher movements in prices. This continued until, with the failure of the Summer Plan, the indexation that had long existed in Brazil cracked because past inflation was no longer seen as a reasonable guide to future inflation and the long-deferred hyperinflation erupted with a vengeance.

Federal Republic of Yugoslavian Hyperinflation (1992-1994)

The Federal Republic of Yugoslavian hyperinflation (Serbia and Montenegro) once again had war serving as the large supply shock. The country began to disintegrate in 1990 when elections in each of the six republics essentially foretold the end of the union. One of the most terrible conflicts seen in modern times ensued as the former Yugoslavia tore itself apart.

In May 1992, the United Nations imposed international sanctions on the Federal Republic of Yugoslavia, which effectively prohibited almost all trade and transactions. The output shock of war and sanctions was enormous, on a similar scale, based on some estimates, to that seen during the Hungarian hyperinflation. As one might imagine, the budget deficit exploded (as tax revenues imploded), rising from 3% of GDP in 1990 to 28% of GDP in 1993. As is often the case (as we have seen above), dollarisation (based on the German mark) of the economy occurred, such that all exchange-rate depreciations created price spirals in the domestic setting.

Georgian Hyperinflation (1992-94)

When Georgia became independent in 1991, it was tightly integrated with Russia and the other members of the former Soviet Union (FSU). In particular, Georgia was a massive importer of energy (gas and refined oil products); its exports were to other FSU states and relied on the railway and road routes to Russia.

The large supply shock underlying the Georgian hyperinflation experience was clearly the break-up of the FSU and its wider impact. The key terms of trade moved sharply against Georgia in 1992 and 1993 as the prices of its key energy imports soared. Added to this nightmare mix were civil unrest and the severing of Georgia’s rail link to Russia. Output collapsed, with a 56% decline recorded between 1991 and 1992.

As has often been observed in the previous examples, the fiscal position of the government deteriorated massively as tax receipts collapsed and expenditure levels were maintained in the face of the terrible domestic situation and import needs. The deficit went from 3% of GDP in 1991 to 26% in 1993. Nearly 80% of the deficit was financed by external loans (or grants).

As the ruble zone ceased to exist, the Central Bank of Russia stopped supplying bank notes to the FSU states, so Georgia introduced the coupon in April 1993 and it became the sole legal tender in August of that year. The Georgian National Bank had to accommodate the spending by the government, and having exhausted its foreign exchange reserves, the currency began to depreciate massively.

As in many of the other instances of hyperinflation outlined above, this created an exchange-rate-driven inflation. As the IMF put it, “The market exchange rate depreciation led the price index change during the hyperinflation period,” just as Helfferich had argued so many years prior with respect to the Weimar Republic hyperinflation. Dollarisation proved once again to be the key transmission mechanism.

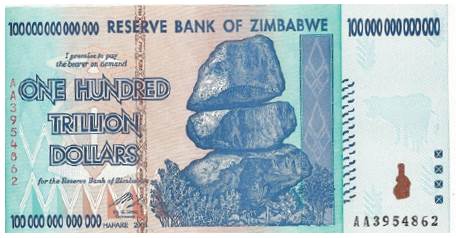

Zimbabwean Hyperinflation (2007-09)

For our final thumbnail, let’s turn to one of the most recent examples of hyperinflation – Zimbabwe. The usual suspects for generating hyperinflation all seemed to play their role here. Zimbabwe began its descent into economic chaos in 1999 when a drought impacted the large agricultural sector. Land reallocation in 2000 and 2001 further increased the supply shock as farms went from those with productive owners to those with little or no interest in farming. Output fell by 50% between 2000 and 2008, with tobacco (a major export earner) dropping 64%, and maize by 76%.

Agriculture wasn’t the only sector to suffer. The infrastructure of the economy was crumbling: the national rail system could no longer transport the country’s mining exports. In 2007 there was a 57% decline in export mineral shipments. Manufacturing was crucified as well, with output falling 29% in 2005, 18% in 2006, and 28% in 2007. The result of this carnage was an unemployment rate of 80%!

The agricultural collapse created the second of characteristics – large debts in a foreign currency. Of course, Zimbabwe already had a large external debt, but this was largely to official creditors, who kept adding the non-payment to the loan itself. However, with virtually no domestic food production, Zimbabwe was forced to import and pay for those imports in foreign currencies.

Given this backdrop, Zimbabwe witnessed large-scale emigration, decreasing the tax base further and worsening the budget deficit situation. Of course, dollarisation of the economy ensued.

Conclusions

13 Keynes wrote his book The Economic Consequences of the Peace in 1919. In it he outlined the dangers posed by the enormous reparations that had been imposed upon Germany.

14 Found in Constantino Bresciani-Turroni’s Economics of Inflation: A Study of Currency Depreciation in Post-War Germany, 1931.

15 Colin D. Campbell and Gordon C. Tullock, “Hyperinflation in China, 1937-49,” Journal of Political Economy, Vol. 62, No. 3, June 1954.

16 Op. cit.

17 Dollarisation is a process whereby a foreign currency replaces the domestic currency. This process makes devaluation of the domestic currency more inflationary faster than it would otherwise have been by creating direct pass-through of exchange rate movements to domestic prices.