Observations Lab

Macro Thoughts

Capital Markets Lab

Asset Management

Markets in History

Beyond Finance

Quotes on the Fly

Chart Gallery

Academia

Latest Observations

Global Financial Data, February 27 2020

Global Financial Data, Aug 14 2019

Yale News, September 22, 2015

Asset Management

Pension Funds

Pension Funds Research

Pension Funds Switzerland

Pension Funds Germany

Pension Funds Denmark

Pension Funds Finland

Pension Funds Norway

Pension Funds Sweden

Pension Funds United Kingdom

Pension Funds Netherlands

Latest Observations

Global Financial Data, February 27 2020

Global Financial Data, Aug 14 2019

Yale News, September 22, 2015

Wealth Managers

The Library

The Chart Room

Quotes on the Fly

The Time Capsule

Beyond Finance

The Coffee Chronicles

The Synchronicity Chamber

The Joseph Schumpeter Room

The Friedrich Hayek Auditorium

The Central Bank Hallway

Latest Observations

Global Financial Data, February 27 2020

Global Financial Data, Aug 14 2019

Yale News, September 22, 2015

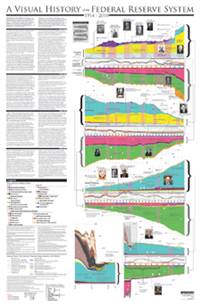

Much of the past decade's history of the Fed remains to be written, but it includes the largest expansion in the Fed’s balance sheet to date, dwarfing the WWI growth of discounts, the 1934 gold revaluation, and the WWII expansion. The expansion’s effect on employment, GDP, credit, and confidence in the dollar continue to play out.

Much of the past decade's history of the Fed remains to be written, but it includes the largest expansion in the Fed’s balance sheet to date, dwarfing the WWI growth of discounts, the 1934 gold revaluation, and the WWII expansion. The expansion’s effect on employment, GDP, credit, and confidence in the dollar continue to play out.