The adoption of negative interest rates will do little to stimulate growth.

Scott Minerd, Chairman of Investments and Global CIO

Guggenheim Partners, April 07, 2016

For the first time since the Great Depression, the world is in a liquidity trap.

The unintended consequence of many central banks pushing negative interest rate policy is conjuring deflationary headwinds, stronger currencies, and slower growth—the exact opposite of what struggling economies need. But when monetary policy is the only game in town, negative rates are likely to beget even more negative rates, creating a perverse cycle with important implications for investors.

When central banks reduce policy rates, their objective is to stimulate growth. Lower rates are designed to spur savers to spend, redirect capital into higher-return (i.e. riskier) investments, and drive down borrowing costs for businesses and consumers.

Additionally, lower real interest rates are associated with a weaker currency, which stimulates growth by making exports more competitive. In short, central banks reduce borrowing costs to kindle reflationary behavior that helps growth. But does this work when monetary policy is driven through the proverbial looking glass of negative rates?

There is a strong argument that when rates go into negative territory it squeezes the speed at which money circulates through the economy, commonly referred to by economists as the velocity of money.

We are already seeing this happen in Japan where citizens are clamoring for 10,000-yen bills (and home safes to store them in). People are taking their money out of the banking system to stuff it under their metaphorical mattresses. This may sound extreme, but whether paper money is stashed in home safes or moved into transaction substitutes or other stores of value like gold, the point is it’s not circulating in the economy.

Japanese Investors Look for Yield Beyond their Shores

The Bank of Japan’s negative interest-rate policy has spurred a run to higher-yielding foreign bonds.

Japanese Investors' Cumulative Net Purchases of Medium- and Long-term Foreign Bonds ($ billions)

Source: Guggenheim Investments, Bloomberg, Japan MOF. Data from 1.2.2015 through 3.25.2016.

The empirical data support this view—the velocity of money has declined precipitously as policymakers have moved aggressively to reduce rates.

A decline in the velocity of money increases deflationary pressure. Each dollar (or yen or euro) generates less and less economic activity, so policymakers must pump more money into the system to generate growth.

As consumers watch prices decline, they defer purchases, reducing consumption and slowing growth. Deflation also lifts real interest rates, which drives currency values higher. In today’s mercantilist, beggar-thy-neighbor world of global trade, a strong currency is a headwind to exports.

Obviously, this is not the desired outcome of policymakers. But as central banks grasp for new, stimulative tools, they end up pushing on an ever-lengthening piece of string. The Bank of Japan and the European Central Bank are already executing massive quantitative easing programs, but as their balance sheets expand, assets available to purchase shrink.

The BOJ now buys virtually all of the Japanese government bonds that are issued every year, and has resorted to buying exchange traded funds to expand its balance sheet.

The ECB continues to grow the definition of assets that qualify for purchase as sovereign debt alone cannot satisfy its appetite for QE. As options for further QE diminish, negative rates have become the shiny new tool kit of monetary policy orthodoxy.

If Dr. Draghi and Dr. Kuroda do not get the outcome they want from their QE prescriptions—which is highly likely—then more negative rates will be on the way.

It would not be a surprise to see the overnight rates in Europe and Japan go to negative 1 percent or lower, which will in turn pull down other rates along their respective yield curves.

Negative rates at these levels would make U.S. Treasurys much more attractive on a relative basis, driving yields even lower than they are today.

If the European overnight rate were cut to minus 1 percent from its current level of negative 40 basis points, German 10-year bunds would be dragged into negative territory and we could see 10-year Treasurys yielding 1 percent or less.

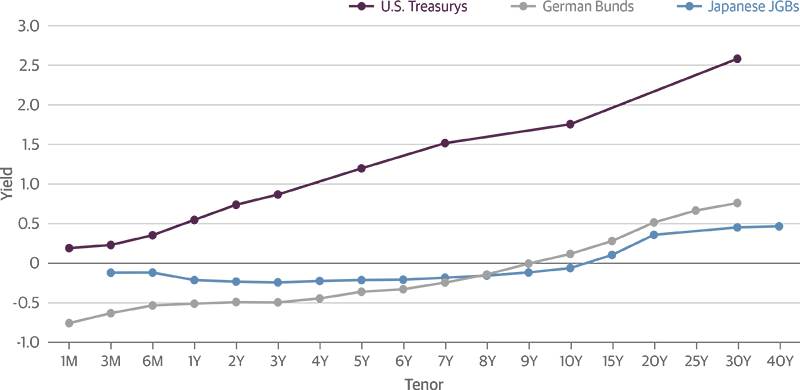

U.S. Is An Outlier Among Global Sovereign Yield Curves

Negative yields in Europe and Japan make U.S. Treasurys much more attractive on a relative basis, and could drive yields lower.

Source: Bloomberg, Guggenheim Investments. Data as of 4.6.16.

This experiment with negative interest rates on a global scale is unprecedented. While there may not yet be enough data to draw the final conclusion about the efficacy of negative interest rate regimes, I have little confidence this will work.

Monetary policy primarily addresses cyclical economic problems, not structural ones. Fiscal and regulatory policies are doing little to support growth, and in most cases are restraining it. Combined with negative interest rates, the current policy prescriptions are a perilous mix that is deepening the global liquidity trap.