“The best way to deal with any economic problem is to let the market work it through.”

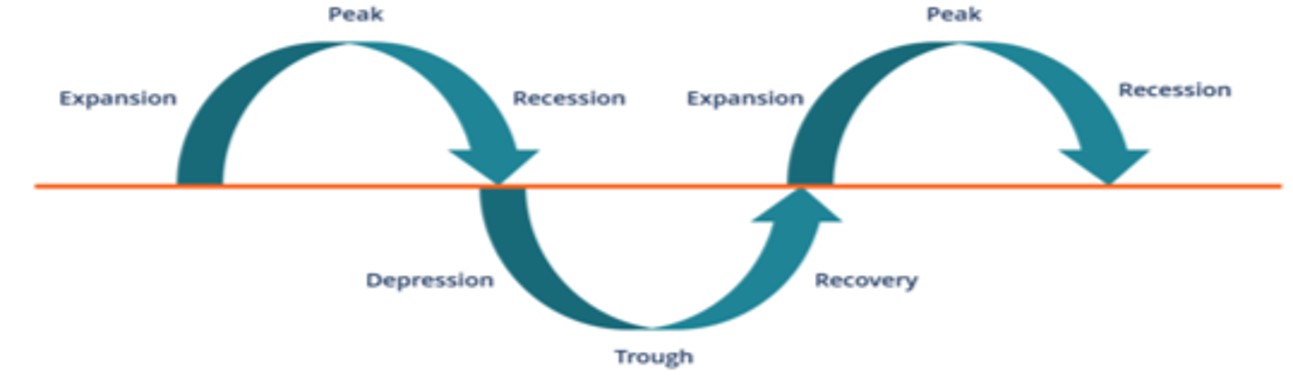

Like seasonal weather patterns, the cycles of the moon or ocean tides, the economies follow a somewhat predictable pattern that broadly alternates between periods of growth (economic expansions) and recessions (economic contractions). Unlike [1] nature’s cycles, however, the timing and duration of the various phases of the economy tend to vary, sometimes substantially, and to the extent that trying to forecast when one phase will end and another begin is more art than science. The challenge is not just in the timing; we also need to consider the secular overlays that impact the cycles over sometimes considerable periods of time. These could range from changes in the degree of secular growth rates over different periods, to the amplitude of the cycles themselves or the duration of the peaks and troughs.

Recent data appears to show a gradual dampening in the amplitude of cycles [2] , but how do we know that this is for real and not just a fluke? Climate change, for example, is backed by a multitude of “smoking guns”, various hard evidences that are almost impossible to refute, let alone argue given the substantial time frame over which the trends and patterns have been taking place. Unlike with the weather, the “shallowing” of economic cycles is more of a recent phenomenon, and therefore belongs more in the realm of a hypothesis in need of additional hindsight and hard evidence to back it up. There are a number of underlying forces that appear to be influencing the shape and form of economic cycles in a manner that does warrant further investigation. They include demographics, technology and the economy.

We all know, for example, that as economies progress and mature and as wealth trickles down to the masses, birth rates begin to decline precipitously, causing an eventual inversion in the shape of a country’s demographics as the ageing cohort begins to swell up in contrast to the newcomers. Developed economies are at the very mature end of this cycle, which means that a greater number of the population (the so-called baby boomers’ cohort) are exiting the workforce than those that are entering it. Of course, technological progress, which includes robotization of certain processes, compensates manual labor to some extent for the void left from a shrinking workforce, which means that output will be less impacted than if it was not the case. A shrinking population in itself does affect growth by reducing the aggregate demand for goods and services, which is also why global trade is so crucial to the equation.

Then there is the cognitively induced evolution of the economy through the ages to consider. The Neolithic revolution some 10,000 years ago brought about the agriculture based agrarian societies, and was eventually superseded by the industrial revolution and its manufacturing-based economies. Manufacturing eventually moved to the lesser developed markets, making way for the service industry in developed economies. It now appears to be in the midst of another transformation, one based on information, brought about by the accelerating effects of the so-called “digital revolution”. These structural changes in the economy are likely profoundly affecting the shape and size of the cycles themselves, most significantly through the effects of technologies that are singularly accelerating the process of almost everything in our lives [3]. Firms, for example, are becoming far more efficient with their inventories thanks to access to ever more sophisticated production chain and stock management tracking systems. In a world where time is of the essence, an almost instantaneous view of the business can give managers the ability to take decisions and make crucial adjustments over shorter time frames.

The digitization of currency, increasingly efficient payment systems and faster communication networks not only mean that financial markets can react quicker to new information, it also further leverages a central bank’s ability to impact the markets themselves. Digitization shrinks response times but also opens new pathways of influence [4] . Logic would dictate that with more information of a higher quality that is more readily available at our disposal and with quicker response times, it should be easier to stop a fire dead on its tracks. This might explain why going forward, contractions are likely to be less severe than in the past, just as the ageing populations and maturing economies might also be dampening expansions.

If we are indeed heading towards “shallower” cycles, the implications of such secular changes could be profound for the investment community and beyond. Less vigorous expansions spread over longer periods would entail a fundamental change in the risk/return dynamics of markets and a resulting shift in expectations. Pension funds, for example, would have to recalibrate their asset expected returns to correctly match them with their liabilities. If shallower cycles also lead to diminishing volatilities [5] , the implications could be even more profound, touching on broader aspects of the financial markets, such as the pricing of options.

Where Do We Go From Here?

The probability of a major global downturn comparable to the last one is slim, namely because both the fundamentals and the dynamics in this cycle are both very different from those of the past. The likelihood of further deceleration in the global recovery and greater volatility in markets, however, appear to be substantially heightened, not only due to a material paradigm shift in geopolitics (the emergence of protectionism and populism over the recent past), but also because of structural changes in demographics, the diminishing productivity rates, not to mention the substantial displacements and other as yet unpredictable effects of technological advances [6] .

Global growth is likely heading towards a secular downshift as a result of an interplay between these various forces. If much of the world has settled to a lower growth equilibrium, it might explain why the current tightening bias of central banks are causing jitters in the markets. It might be that the neutral rate for interest rates is at a lower level than previously, which would mean that Fed tightening is actually pushing growth dangerously into the deceleration zone. Global signs of an economic slowdown, heightened volatility and recent corrections in the markets have prompted key central banks across the globe to take a step back and reassess the broader outlook. The Fed has hinted that it might take a break from further tightening, the ECB looks like it will revert back towards accommodation, whilst China’s central bank takes concrete steps to stimulate bank lending.

Faced with the Brexit uncertainty, France’s endless street protests, a steadily deteriorating economic climate (Italy) and the migrant-fueled growing political rift between member states, Europe’s prospects appear increasingly grim. Decision-making is likely to be further hampered and the existential threat may take on a more virulent form after the May EU parliamentary elections, especially if populism-tinged parties gain a stronger foothold in parliament [7] . Such an outcome will create additional headwinds for a floundering economy in need of heightened guidance and leadership to steer it out of the doldrums. The ECB’s president will also be stepping down in October. With his successor still to be determined, this will be another source of uncertainty for the markets for most of the rest of the year.

For the U.S. economy the main source for headwinds will continue to originate from the uncertainties brought about by an erratic leadership and its damaging protectionist policies. This will continue to have a dampening effect on both investments and consumption over the longer haul, which will be further compounded by the diminishing stimulus effects of last year’s tax cuts and the sharp rise in oil production investments as oil prices remain lower. The Fed will likely take a pause from its tightening spree but will remain under pressure to resume building its stimulus reserves at the earliest opportunity. Further tensions with China and other strategic partners and foes will erode confidence in the global world order, which will open yet another front of instability for the markets.

China’s economic slowdown will be increasingly difficult to counter, let alone steer. The expansion will likely settle in the 6% range, a far cry from the 10% average achieved over the previous three decades. The massive debts that China has accumulated from the last global financial crisis, as it countered it with major stimulus injections into the economy, will limit the government’s room for maneuver in this cycle[8]. This will be compounded by ongoing trade barbs with the U.S., tariffs on a broader range of exports and retreating household consumption as wages soften and debts continue to rise. Still the Chinese government has considerable reserves which it may have to resort to if the situation wih the U.S. deteriorates further.

A liquidity infused era is ending, the “band-aid” is being gradually peeled off, revealing a more natural form of the cycle. A cycle that appears to have changed in shape over the years, the result of various forces that have been gestating, affecting it at its core. In the meantime, global growth is slowing down, time will reveal the exact nature of this, but one thing is for sure, a more toxic political climate will worsen matters. Indeed, there is nothing worse to our cognition than uncertainty.

[1] To be fair, weather patterns are becoming increasingly unpredictable given the long-term effects of human-induced climate change. Winters appear to occur over shorter periods but with greater intensity, whilst summer temperatures continue to break records and extend over longer periods than in the past.

[2] https://blogs.cfainstitute.org/investor/2018/12/20/the-changing-nature-of-recessions/

[3] Unlike the big manufacturing firms of the past, some of the most valuable companies today are in the business of shuffling data spread across server farms. Duplicating and distributing a piece of digital software is easier, faster and less costly to accomplish than it is producing a car, even one built by Tesla.

[4] The massive, coordinated central bank liquidity drive, not to mention the whole quantitative easing process that shortened and limited the depth of the last financial crisis, would have been impossible without the technological changes in recent decades.

[5] Greater speed and efficiency in communication and action may not necessarily lead to an absolute drop in volatility rates; we still need to consider the unknown variables of cognitive behavioral biases and the concentration of wealth that both have the potential of moving markets and therefore volatilities considerably.

[6] The International Monetary Fund still thinks the global economy will grow a respectable 3.5% this year. But that is the second downgrade from a year ago when the IMF hailed “the broadest synchronized global growth upsurge” since 2010.

[7]https://www.theguardian.com/commentisfree/2019/jan/25/fight-europe-wreckers-patriotsnationalist

[8] China’s economy has been decelerating partly due to President Xi Jinping’s initiative of the past three years to contain debt and fend off financial risks. That campaign has curbed borrowing by local governments and businesses and caused a sharp fall in spending on new subway lines and factories.

This document has been produced purely for the purpose of information and does not therefore constitute an invitation to invest, nor an offer to buy or sell anything nor is it a contractual document of any sort. The opinions expressed are those of the author which do not necessarily coincide with the views held by Lobnek Wealth Management or its affiliates. No part of this publication may be reproduced or distributed in any form or by any means, or stored in a database or retrieval system electronic or otherwise, without the express prior written permission of the author