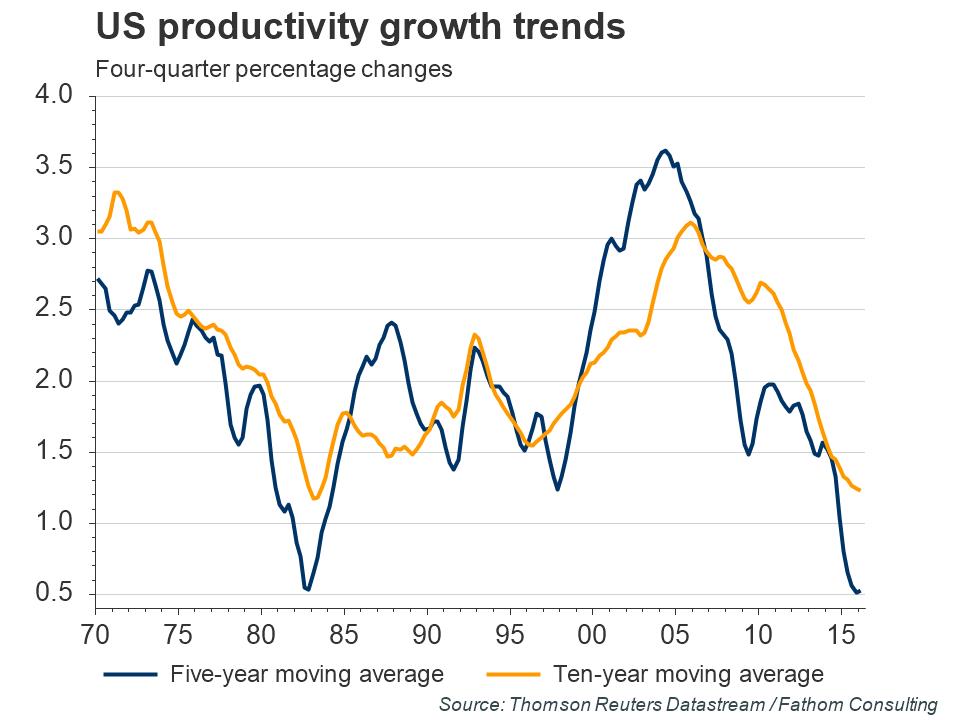

Although in relative terms the US has had a good recovery, in absolute terms it has not. (...) Whether we look over the past five years, or whether we look over the past ten years, US productivity growth is close to as weak as it has ever been.

Fathom Consulting, June 10th 2016

Although US labour market productivity in the first quarter of this year was revised up on Tuesday, broader productivity trends remain a concern. Janet Yellen expressed her worries about this in a speech this week and wants politicians to do more to encourage greater spending on investment and education. In our view, the policy mix should shift towards greater fiscal stimulus in the years ahead. That is because we believe that ultra-loose monetary policy is now causing more harm than good. Indeed, our analysis finds that low interest rates may be preventing the ‘gales of creative destruction’ that typically boost an economy’s potential supply in the aftermath of a recession.

Speaking with her three surviving predecessors back in April, Federal Reserve Chair Janet Yellen defended last year’s 25 basis point increase in the federal funds rate, the first for almost a decade. She was adamant that the tightening was warranted, and that no mistake had been made. We agree. And while she praised the “tremendous progress” made by the US economy since the depths of the financial crisis, one important qualification remains: productivity growth is worryingly sluggish.

Although Tuesday’s data contained upward revisions, productivity growth remains very low by historical standards. Indeed, the revised annualised growth rate of productivity within the nonfarm business sector was still negative in Q1, at -0.6% versus the earlier estimate of -1.0%. And this followed a contraction of 1.7% in Q4! Admittedly, Q1 productivity was 0.7% firmer than in Q1 last year, but that rate of growth is a lot lower than the historical average of around 2.0%. We think that this is because interest rates have been too low, for too long.

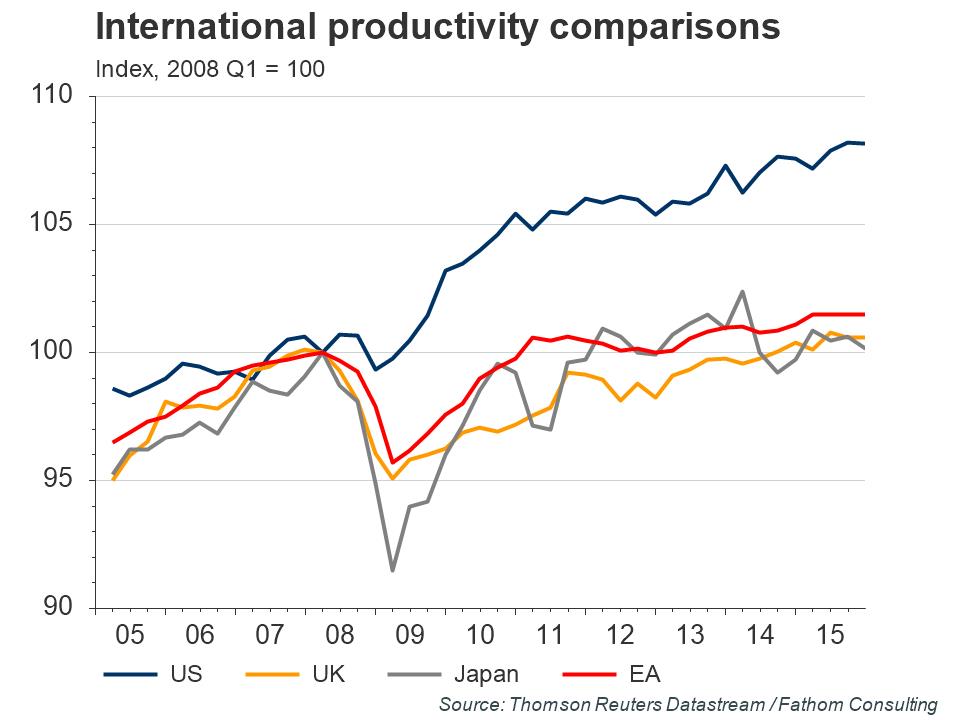

Alone among those economies that suffered a severe banking crisis through 2008 and into 2009, the US moved swiftly to recapitalise its own deposit-taking institutions. That was progress indeed. It is why US banks are lending again, and it is why, in productivity terms, the US has outperformed more or less every major economy since the Great Recession came to an end. Although in relative terms the US has had a good recovery, in absolute terms it has not. Our second chart shows that US productivity growth tends to move in long cycles of booms and busts. Whether we look over the past five years, or whether we look over the past ten years, US productivity growth is close to as weak as it has ever been.

In the words of Nobel prize-winning economist Paul Krugman “Productivity isn’t everything, but in the long run it is almost everything”. With demographics largely beyond the control of policymakers, it is effectively productivity growth that determines an economy’s sustainable rate of economic growth, and by extension the long-run returns to a broad range of financial assets. Consequently, understanding the causes of historically weak rates of productivity growth across the developed world is of particular importance to investors.

In putting together our latest global forecast, we spent some time trying to account for the variation through time in US productivity growth. Our suspicion was that low rates of productivity growth post-crisis were in some way related to the policy response to that crisis. By cutting interest rates almost to zero, central banks around the developed world were able to stave off a wave of corporate failures. Empirically, peaks and troughs in the US federal funds rate lead peaks and troughs in the US corporate failure rate by two to three years. This is not rocket science. But what if the corporate failure rate in turn affects productivity growth? Our research suggests that it does.

We found that we could explain more than two thirds of the cyclical variation in US productivity growth using just three variables. Specifically, we found that US productivity growth rises with the US corporate failure rate, falls with the level of the real oil price, and rises when output is growing faster than potential. By modelling the relationship between the federal funds rate and the corporate failure rate, we found that the reduction in the federal funds rate from its pre-crisis average of 4¼% almost to zero could have shaved around a percentage point off the rate of growth of US productivity. By keeping a lid on corporate failures, the Federal Reserve, along with many other central banks around the world, may unwittingly have prevented the ‘gales of creative destruction’ that typically boost an economy’s potential supply in the aftermath of a recession.

If we are right, then Chair Yellen and her team might do well to knuckle down and get on with delivering higher interest rates. Following the surprisingly weak non-farm payrolls data for May, which we regard as a ‘blip’, a June tightening is probably off the table. But if, as we suspect, we see a strong non-farm payrolls figure in June then a tightening next month is still on the cards.