Key Points

This report argues that cryptocurrencies are technology solutions in search of a problem. Paradoxically, despite the libertarian overtones, governments and Central Banks are likely the main beneficiaries of DLT (distributed-ledger technology). They will provide e-monies to the public, replacing high street banks in the payment mechanism. High street banks are the dinosaurs.They will face further competition from specialist lenders for credit provision and money market funds for deposit-taking. Ultimately, gold and Central Bank money will prove more important for the future monetary system than cryptocurrencies. They are a fad.

Key Points

- blockchain and Bitcoin are questionable new technology solutions desperately seeking a problem. We explore the future through the four 'prices' of money

- Be warned, crypto-currency prices may soon collapse

- Money requires low cost informational efficiency and stable value. Bitcoin (i.e. ¼value¼ question because of e.g.‘forking¼) and blockchain (i.e. time and energy cost issues), despite its informational efficiency, fail to provide monetary solution. Blockchain should have other advantages?

- Need to distinguish cryptocurrencies (e.g. Bitcoin) from blockchain (i.e. linkages), and blockchain from the distributed-ledger technology (DLT, i.e. the network). The Distributed ledger technology (DLT) will empower Central Banks

- Central Banks paradoxically are the main beneficiaries of DLT and will dominate future monetary system with national e-monies, (e.g. e-dollars, e-pounds)

- Money market funds will compete for deposits, and, in turn, fund specialist lenders (e.g. car finance, mortgages, student loans)

- High street banks are the dinosaurs: wholesale money markets and specialist lenders will replace them

- Credit risk will become more explicit in future and pose financial stability questions

- Gold and Central Bank Money will prove more important in the future than cryptocurrencies

What are the Cryptocurrencies?

Cryptocurrencies are all the rage, but be warned prices may soon dive. They may not be a fraud, but they are certainly a fad. Admittedly, cryptocurrency prices have recently soared, pushing their total market value to US$452 billion2, up from US$22 billion a year ago – a remarkable 20-fold leap. The crypto-market is not just chaotic in price terms since the number of units traded has itself nearly tripled from 584 to 1531, while spot trading of these “coins” occurs on more than 400 on-line exchanges around the World. Topping the list is Bitcoin (US$185 billion); Ethereum (US$84 billion) and Ripple (US$35 billion). These three key units account for more than two-thirds of the entire cryptocurrency universe by value. (A year ago, the top three made up an ever larger 94%). But they seem somewhat less popular on Main Street, since in 2016 only five of the Top 500 US retailers accepted Bitcoin and last year this dropped to three!

1 Based on a speech given at the House of Commons, Macmillan Room, March 5th 2018

2 Source: CoinMarketCap.com (2/3/2018)

What’s more, contrary to what one might expect, the demand for old-fashioned cash is still growing. The total value of Bank of England notes in circulation recently peaked at over £73 billion, an increase of 8% on 2016: similarly in the US note usage is growing at a 7.4 annual clip. Some 2.7 million people in the UK, 5% of all adults, spread evenly across age cohorts, rely almost entirely on cash to make their day-today payments. And, in the wake of last September’s Caribbean storm-damage to power supplies and communications, Puerto Rico became what The New York Times described as a ‘cash-only island’. To cope with the extraordinary demand, the US Federal Reserve even had to fly in extra notes and coins.

Formally-defined, a cryptocurrency is a digital, encrypted asset designed to work as a means of circulation, using cryptography to secure the transactions and to limit additional supplies of the currency. It is mathematically-based and programmers around the world use freely available software algorithms to produce the cryptocurrencies. In essence, cryptocurrencies enable secure peer-to-peer transactions, without any need for either intermediaries or a trusted Centralised Authority. On paper, they would seem to be an anarchist’s dream?

Cryptocurrencies rely on blockchain, the popular name for the distributed-ledger technology (DLT) that powers the issuance of Bitcoin. Historically, ledgers have always been at the heart of economic transactions, but recently highspeed computers have allowed vastly bigger and more efficient record-keeping and ledger maintenance. Today, computer information is rapid, decentralized and cryptographically-secured. Whereas blockchain focuses on how data is stored and linked to one another in a chronological manner within blocks, a DLT focuses on the sharing of the database amongst all the operating participants of the network. Across the World, corporations from a wide range of industries, from logistics to pharmaceuticals, are looking into the wider ‘disruptive’ potential of blockchain, which, at the same time, seems to offer particularly exciting potential for the monetary and financial sectors.

One key difference between a conventional transaction and one conducted through blockchain concerns the contracting parties. A conventional trade only needs two parties, who enter into and jointly verify a contract, governed by mutually-agreed terms and conditions. No other party (apart from a facilitating intermediary, such as a bank) is required to execute each contract.

In contrast, a blockchain transaction not only involves the transacting parties, but embraces every member of the network as well, and each member must validate every transaction before it can be executed. Their multiple signatures allow a transaction to be accepted by the network, conditional on the approval of a certain number of agents from a pre-defined group. Each change, once approved, is immediately reflected in every subsequent copy of the ledger. All Bitcoin transactions must be public and transparent, because, without this blockchain system, an anonymous cryptocurrency transaction would unlikely be accepted by the market. Because the network validates every ledger entry by consensus, there is supposedly no longer any need for an intermediary to guarantee or police its security and validity. The details of every network transaction that ever happened in each blockchain are stored (and possibly other more questionable information, as well), which means that Bitcoin, for example, is not strictly anonymous because anyone can view the balance and transactions history of any address. However, the identity of the Bitcoin user behind an address, in theory, remains unknown until information is revealed during a purchase or in other circumstances. The blockchain network assures the transacting parties that the underlying cryptocurrency exchange is genuine. It also means that cryptocurrencies are independent of any Central Authority. Bitcoin allows banks,businesses and individuals to securely send and receive payments anywhere and at any time. Supposedly, anyone is allowed to set up a Bitcoin address in minutes, with no questions asked and with no fees payable: surely, a criminal’s dream?

On the other hand, despite their technical merits, cryptocurrencies seem unlikely to either be widely-used or even become part of a mainstream investment portfolio or national monetary system anytime soon. The crypto-markets are highly volatile, fragmented, largely unregulated, and they come with unique liquidity and operational risks, as well as high costs. Bitcoin’s price surge towards US$20,000 in December 2017 highlights that the value of cryptocurrencies experience such wild swings that they fail to meet a key requirement of ‘money’ – that it offers a stable store of value. Compare the annualized daily price volatility of the main cryptocurrencies to US stock market prices and gold. The annualised volatility of the cryptocurrencies (Ripple 170%, Ethereum 140%, Bitcoin 80%) dwarfs that of US equities (15%) and gold (18%), and makes the gyrations of Wall Street (31%) during the 2008 Global Financial Crisis even look tame by comparison.

On top of these dramatic price swings, cryptocurrencies also face major challenges such as weak regulation and security flaws at cryptocurrency exchanges and other end-points, e.g. two recent well-publicised cases of over US$1 billion lost by fraud (i.e. MyBitcoins and Mt. Gox). Valuation is difficult, as crypto-assets have no cash flow, earnings or interest rates. Their uses vary from being a speculative bet to the demand for a payment medium. Regulators and Central Banks also need to play a bigger role, e.g. Governor Mark Carney’s recent BoE speech. And a global regulatory framework may be in the offing because ‘How to regulate the cryptocurrencies’ is on the agenda of the March 2018 G20 meeting.

What’s more, while its transaction fees appear to be minimal, Bitcoin’s operating costs are sky-high. For example it costs roughly 2 cents to process each cash transaction, 12 cents per credit card and 26 cents per on-line transaction. This compares to US$2.80 for a blockchain settlement, which itself takes at least 10 mins to verify and sometimes hours. Industry estimates claim that the blockchain system can currently settle at a rate of seven transactions per second. But this compares to the major credit card companies who settle upwards of 65,000/ second, and then by using only around ½% of the energy required for blockchain.

Most new Bitcoin ‘mining’ and verification takes place in China, using coal as primary energy. Assuming an electricity price of 5c per kWh, this means that each Bitcoin eats up about 150 megawatt-hours of electricity. Under its current rules, Bitcoin permits the mining of 1,800 new coins a day, implying daily use of 24,000MWh or an annual rate of nearly 100TWh – about 0.3% of total global electricity use. Put differently, the most widely-cited estimate of this energy requirement compares it to the electricity usage of New Zealand, but even this may be an underestimate. Looking ahead, in order to shift the entire global financial system to Bitcoin would require at least a 2000-fold increase in its energy-use, which, in turn, would entail boosting the World’s entire electricity production by an amazing five-fold!

What Is Money?

Aside from this obvious impracticality, the economic case against cryptocurrencies as ‘money’ may be even more damning? The history of money is the evolutionary path from a simple commodity into what Classical monetary theorists dubbed a universal equivalent. Money and other similar financial assets possess two key properties: (1) information regarding ownership/ title, and (2) value. The winning characteristic of money is its ability to radically reduce the amount and cost of information required to intermediate each transaction, while at the same time maintaining its value. Historically, this ownership question is straightforward when money is in bearer-form, and value, in turn, is closely-related to unit supply. Throughout history, the value question has often been paramount since money is used to settle debts.

This requires it to be: (1) a standard of value, which effectively means: (a) being a store of value, and (b) (officially as ‘legal tender’) recognised as a unit of account, and (2) a means of circulation, which means being accepted as a standard of value by both parties to a transaction.

First, what are these transactions? They can be divided into three categories: (1) conventional economy; (2) ‘legal’ black economy, e.g. casual work, and (3) ‘illegal’ black economy, e.g. crime, tax evasion, money laundering and drug dealing. The arguments in favour of cryptocurrencies simply cannot rely on the latter. Moreover, users of Bitcoin have no control over its security or its issuance, e.g. it is not bearer and can get ‘forked’, e.g. the surprise appearance of Bitcoin Cash (see: Carstens, BIS, 2018). And, assuming, as seems likely, that in practice blockchain is not anonymous, the authorities may prove able to track transactions, making tax evasion and money laundering far more difficult. All this means that it is hardly the ideal libertarian solution.

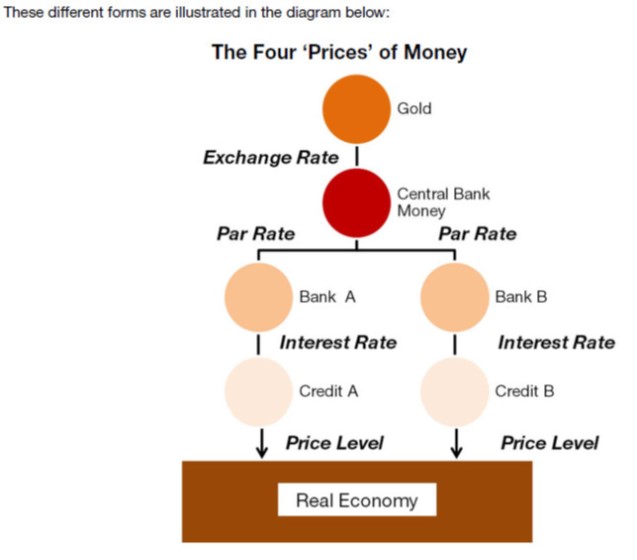

Second, what type of traditional ‘money’ could Bitcoin and blockchain replace? This is the trickier question because, in practice, money appears in four different forms in the modern economy:

1. Gold/ ‘universal equivalent’, where its ‘price’ is the exchange rate

2. Central Bank Money, where its par ‘price’ ensures that, say, the ‘HSBC pound’ trades 1:1 at parity with both the ‘Barclays pound’ and the ‘Bank of England pound’

3. Bank Money, or credit money, where the ‘price’ is the interest rate

4. Transactions Money, where the ‘price’ is the high street price level

What is the Digital Future?

The obvious monetary advantage of blockchain is that it stores ownership information efficiently, albeit at a high extraction cost, but it is less clear how the ‘value’ question is answered. This implies that blockchain may be nothing more than a useful ‘back office’ function? The value and, hence, the supply of cryptocurrencies is connected to the existence of net payment surpluses in their respective blockchain networks. New supply often depends upon some form ‘verification’ but, as we now know, this is costly in both time and resources, and does not prevent ‘forking’. Moreover, set against a hazy notion of demand for the cryptocurrencies and an entirely unclear future supply, it remains uncertain how they can achieve anything close to stable monetary value.

On the other hand, distributed-ledger technology (DLT) paradoxically offers huge attractions to the existing Monetary Authorities in helping them digitise their existing monies. The Swedish Riksbank, for example, is currently looking at ekrona, but it has also explicitly ruled out a blockchain settlement solution. Rather what is likely to evolve is a future where every citizen holds e-monies in a secure wallet at their respective Central Banks. This single digital ledger, in economist’s jargon, describes a narrow banking model, much like Peel’s 1844 Banking Act in the UK that legally split the Bank of England Issue Department from the Banking Department in order to more clearly identify the gold backing for the note issue. With a recognised central authority policing settlement, the plodding and costly blockchain verifications can be easily swapped for instantaneous and cheaper digital settlements. These e-dollars and e-pounds simply become the digital equivalent of paper notes, but available via, say, smartphones. (Note that alongside this emoney, notes and coins may still physically exist.) The net balances of e-money will attract zero or low interest rates from the Central Bank. (Note that the Bank of England has proposed the possibility of ‘negative’ interest rates on these eaccounts to further improve its monetary control and so stimulate spending.) Excess funds can be instantly scoopedoff and recycled through the wholesale money markets, where they are either relent by specialist lenders or used to buy securities. These credit providers will use this funding to lend into the specific areas that they are experts on, such as car finance, student loans and mortgages. This will mean that the future monetary system will become more disaggregated, more specialised and, ironically, may again look much like it once did in the nineteenth century.

Central Bank money will still needed by both the private and public sectors. The private sector will demand a ‘safe’asset it can rely upon and the State still needs to pay its bills. Put another way, controlling the price and quantity of money will remain a necessary and a very profitable business because of seigniorage (‘…the right of the lord to mint money’). The future supply of Central Bank money will face its usual tensions, such as the need to cover government spending deficits and the ad hoc provision of liquidity to markets during crises. What remains unclear are potential systemic risks and the resulting demand for this ‘safe’ asset, since with the future financial system more disaggregated and credit risk more explicit, the choice of assets in crises may become binary, so requiring huge provision. As before, the vent for these liquidity surges will be the forex markets. E-monies will, therefore, not stop future currencies devaluing against gold. In fact, perhaps, the World is ultimately turning full-circle back to gold?

The dinosaurs out there are what we term ‘bank money’ and the traditional high street banks. They face extinction. Traditionally, these banks developed as ‘safe’ places to physically deposit cash, with safety determined, first, by the quality of the assets that ‘secured’ their deposits and, second, by their unique access to Central Bank funding in extremis. These advantages effectively allowed the commercial banks to create money at will, since the State effectively guaranteed their deposits. Put differently, all modern money is credit, and whereas in the 19th century private banks, of varying reputation and quality, issued their own bank notes and promissory notes, today the cheque is the modern equivalent, whose acceptability depends entirely on the issuing banks’ perceived credit rating.

Thus, the notional ‘Barclays pound’ today exchanges for the same as an ‘HSBC pound’ because of these State guarantees. We have labelled this in the diagram the ‘par’ price of money. It is this par price that is likely to breakdown in the future, since it seems unclear why the State would continue to underwrite banks’ deposit liabilities? In this new World, a commercial Bank failure is unlikely to disturb the payment function of money because this will be exclusively handled by the Central Bank, but it still may affect credit provision. In other words, in the new digital World, credit risk may become a more obvious feature of banking and deposit-taking.

Conclusion: Lonely Bytes – A Technology Solution Desperately Seeking A Problem

‘If it ain’t broke don’t fix it’ is, maybe, the final comment on the cryptocurrencies. They seem to be a technology solution desperately seeking a problem. Essentially, to understand the issues, DLT (the network) needs to be thought of separately from blockchain (the linkages) and, in turn, both need to be distinguished from cryptocurrencies (the net payment surpluses per network). We conclude that cryptocurrencies are likely a passing fad, but one that may spawn a very different financial revolution that puts the Central Banks firmly in control and sees the disappearance of the traditional high street banks? Central Banks are the one institution that seems most needed and which potentially benefits most from the distributed-ledger technology (DLT). In this report, we argue that only one of the two key monetary puzzles – information efficiency and stable value – can be solved by blockchain, albeit at a high cost in terms of time and energy-use, while its associated cryptocurrencies, like Bitcoin, fail to adequately answer the value question, in part, because of the potential for ‘forking’. Here, in terms of money provision, the State will remain dominant. Although the gold price remains an established barometer of our distrust in governments, they have effectively demonetized gold within their jurisdictions, and they will similarly successfully demonetize the cryptocurrencies. Governments need tax revenue and fiat currencies, and the control of money is a vital part of economic policy and, in the Modern World, an expression of sovereignty. Governments may prevent taxes being paid in Bitcoin, but they may still use the transparency of blockchain to assess them. They will force transactions to be denominated in national currencies for tax collection reasons and ban Bitcoin, when necessary. Take your choice, will this be Big Bank or Big Brother?