Interesting comments and charts from an external member of the Bank of England's Monetary Policy Committee.

Speech given by David Miles

Bank of England, Speech, June 26th, 2013

Excerpts from a speech given by David Miles at the Global Borrowers & Investors Forum, London, 26 June 2013:

"The nature of the effects of large scale asset purchases by central banks is controversial, important and of immediate relevance to policy. I want to consider the evidence on the impacts of such asset purchases, assess whether they are causing distortions in financial markets – rather than provide support for demand in the wider economy – and offer some thoughts on how the exceptional setting of monetary policy we see in the UK today might ultimately be normalised."

...

"Much of the most vocal and opinionated analysis of the impacts of central bank asset purchases – quantitative easing (QE) – strikes me as somewhat contradictory."

...

"Some people seem to believe that large scale asset purchases by central banks have created a bubble in many asset markets and that stopping such purchases (let alone reversing them) must cause big falls in prices. Others take the view that these central bank purchases are ineffective in stimulating demand in the wider economy. I think the evidence for either of these positions is weak. But some people believe both things – a position that I think is also contradictory as well as being profoundly pessimistic."

...

"I want to look at that evidence and also think about what the impact on the wider economy is of asset prices having been held up relative to where they might have been. I also want to look ahead to think about what might happen when monetary policy is once again normalised."

...

"I do not think we should be in any hurry in the UK to move the monetary policy dials back to more normal settings – indeed it might well be right for the next move in the UK to push them even further to give more support to demand."

Asset purchases and bubbles

"I think the claim that QE has artificially boosted the prices of many assets to bubble levels does not stand up. But it is true that in purchasing financial assets central banks – certainly the Bank of England’s Monetary Policy Committee – have deliberately and consciously raised the demand for these assets and that will have supported their prices."

...

"Supporting asset prices helps to support growth, because it means that many companies find it easier to raise funds and because it means that household borrowers face lower longer term interest rates. By keeping the value of portfolios of wealth higher than they would have been the spending of many people who own that wealth is supported. Does anyone doubt that many households who, even given the recent sharp sell-off, have seen the value of their ISAs and other stocks and bonds rise over the past few years would have been less inclined to spend had these savings instead fallen sharply in value?"

...

"There is a world of difference between supporting asset prices so as to prevent a self-reinforcing downward spiral in

values and creating a bubble. Indeed preventing a downward spiral – because it stabilises both asset prices and the wider economy – is pretty much the opposite of blowing up a financial market bubble. The evidence for a general bubble in asset prices is not very convincing. Before the very recent sharp falls, stock prices had risen strongly over the past year or so. A couple of weeks ago the FTSE All-Share index was about back where it was in the summer of 2007. (...) In real terms stock prices were at about the average level of the past 20 years. "

...

"Price to earnings ratios on those stocks do not look unusually high. (...) PE ratios are currently significantly below the average in the ten year period leading up to the crisis of 2007-08."

...

"Were there to be a bubble in stock prices I would also expect the equity risk premium – the gap between expected returns on a portfolio of stocks and on safe bonds – to have declined to exceptionally low levels. Although we cannot measure the equity risk premium accurately, estimates based on a dividend discount model suggest the risk premium on stocks in the FTSE index is actually substantially above the average of recent decades."

...

"What about UK house prices? Average house prices in the UK are – according to some national measures – only 5-10% lower than at the end 2007 peak. Different indices of house prices tell somewhat different stories. But in real terms, that is adjusted for the general rise in the price of goods, they are all down very substantially. Some measures are down by about 30% in real terms; some are down by about 25%; some measures of house prices in England and Wales (which exclude Northern Ireland where prices are down dramatically) are, in nominal terms, more or less where they were at the end 2007 peak – but even they are some 20% lower in real terms. Deflating house prices by an index of disposable incomes shows much the same picture: average house prices relative to average disposable incomes are down by between 20% and 30% from peak levels."

...

"Yields on UK government debt – both in nominal and real terms – are unusually low (Figures 6 and 7). That is true even after the recent sharp sell-off in gilts following re-assessment of the Fed’s likely scale of asset purchases. Part of the low level of gilt yields reflects a belief that the Bank of England is likely to keep Bank Rate at relatively low levels for some time yet. Part of it is likely to reflect a substantially higher perceived level of risk now relative to before the financial train wreck of 2007-8. That puts a premium on relatively safe assets like gilts. So there are good reasons why yields on safe government bonds should be low today. I think some people are far too quick to label this a “bubble” – which I would define as a level of prices far removed from what can be expected given the fundamental economic forces at work in the wider economy."

...

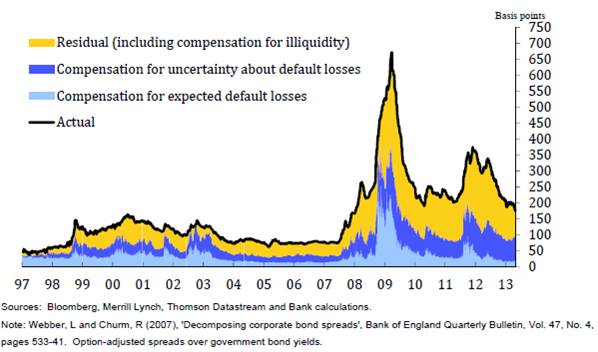

Figure 9. shows a decomposition of that spread which attempts to identify the part due to illiquidity and uncertainty and a part due to expectations of losses on corporate debt. The component due to illiquidity and uncertainty still appears unusually high – suggesting that bond prices still remain somewhat depressed. This is hardly a bubble."

Decomposition of sterling investment-grade corporate bond spreads (Figure 9)

Asset prices and the wider economy

"What is one to make of the uniquely pessimistic, but increasingly widespread, view that QE has both created multiple asset bubbles while having no impact in boosting demand in the economy? What I find implausible about this is the idea that a rise in the value of assets, and a fall in the likely future return on savings, could have no effect on stimulating someone’s spending. You would have to believe that investment was not at all responsive to a greater availability of funding at a lower required return. Is that really plausible?"

...

"Furthermore, it is not clear that the Bank of England’s balance sheet will ultimately shrink to where it had been before the crisis. Banks have learnt that they took excessive liquidity risks before the crisis, and, independently of tighter regulation, are likely to want to hold substantially higher levels of liquid assets in future. Some of these assets are likely to be held in the form of central bank reserves. A natural asset for the central bank to hold to balance the increased amount of commercial bank reserves are government bonds. So it is very far from clear that returning monetary policy to a normal setting means that the Bank of England balance sheet will shrink back to where it was before the crisis."

...

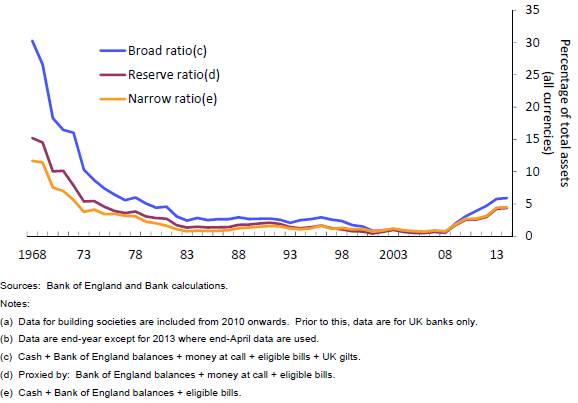

Figure 10 shows just how small were the most liquid of assets held by banks before the crisis. Even now – after a huge expansion of reserve balances held by banks at the Bank of England – levels of the most liquid banks’ assets (reserves and gilts) relative to bank balance sheets are far smaller than was normal in the 1970s and before. Even if banks only went a small part of the way towards holding portfolios of liquid assets that were considered normal some decades ago, they would be holding far more such assets than was the case before the Bank of England started QE and commercial bank reserves increased sharply."

Sterling liquid assets relative to total asset holdings of UK banking sector (a) (b) (Figure 10)

...

"All in all, I think there is a far more plausible, and rather less sensational, view on the effects of QE. This is that it has supported a wide range of asset prices and that this has caused spending to be higher than it would otherwise have been."