Whereas 101 economics tells you to a) curb government spending during good times, and b) boost fiscal policy during periods of hardship (i.e. slowing private demand), most nations did manage to do the exact opposite, or even worse!

That is, they increased government share of GDP when private sector demand was growing , and they reduced public spending when the private sector share of GDP went south; or, in some cases, they increaseed public demand in both growing and shrinking economies. Go figure out!

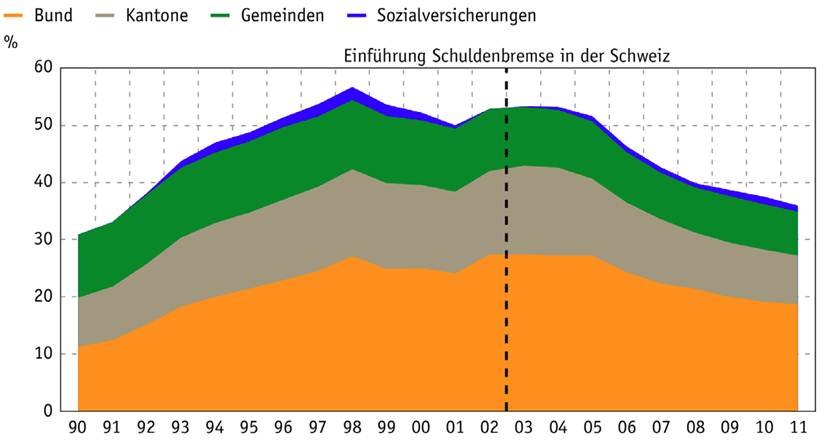

That being said, there are a few exceptions to the rule, Switzerland being the most prominent example. Nothing new so far, but it is good to look back ten years ago, when a few opinion leaders had the lucidity to initiate a process of public debt reduction ( "Schuldenbremse"). The addiction to government spending was effectively reversed in 2003, and it has never looked back since then ! Whether the recent massive currency interventions of the Swiss National Bank could be interpreted as a "hidden" form of public debt, this is food for another debate !

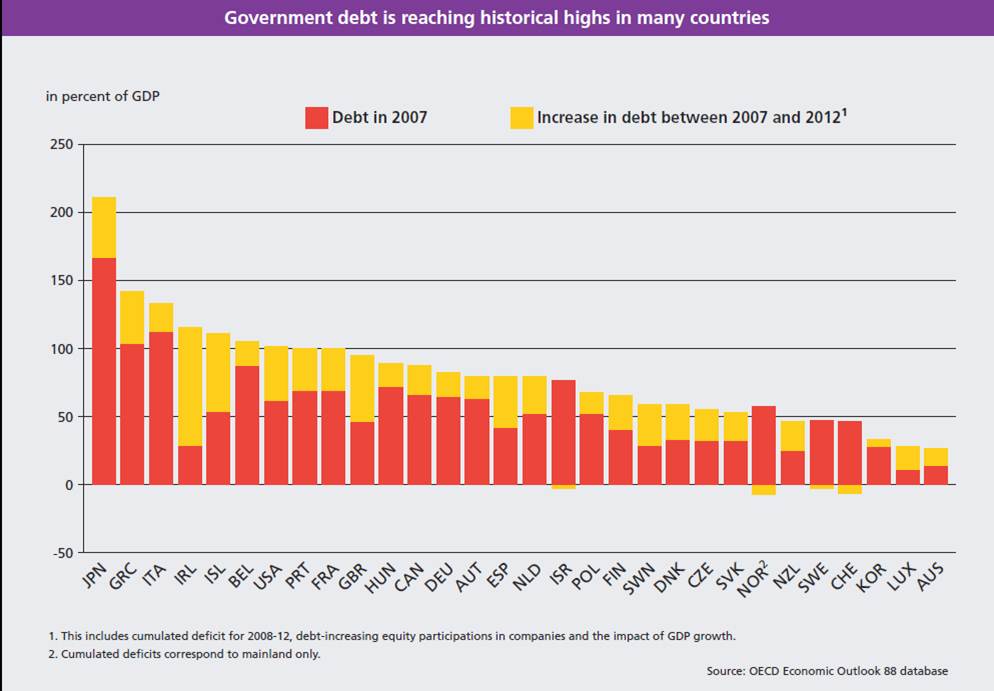

To have a broader basis for comparison you can have a look at the chart below, which shows the evolution of government debt for the OECD from 2007 to 2012. If we exclude Norway, which enjoyed a free rent from the oil boom, Switzerland and Sweden are the two economies that really stand out.