The notion of gold as a hedge against systemic risks is flawed. We believe that the concept of gold’s role as an insurance policy needs to be narrowed significantly.

Amit Bhartia and Matt Seto

GMO, April 2013

Last year(1) we argued that relying on conventional wisdom to analyze gold price movements is naive. Conventional wisdom would lead us to believe that gold price movements are driven solely by the actions of developed markets’ central banks. We believe this view is misinformed and that the available data does not support it.

In that paper, we argued instead that the key driver of the significant rise in gold prices since 2000 has been the emerging markets consumer. Between 2000 and 2010, consumers in emerging markets accounted for 79% of total demand. Conversely, ETF purchases accounted for only 7.5% of demand and central banks in aggregate were net sellers.

This expanded framework demonstrates that gold is also positively exposed to pro-cyclical factors in the emerging markets. Moreover, given the cyclical challenges gold’s key consumers may be facing, the value of gold as insurance should be questioned.

Over the past 13 years, the impact of emerging markets on gold prices was unequivocally positive: emerging markets drove gold prices higher. However, this has not always been the case through history and, we believe, will not always be the case going forward. Emerging markets can be both a positive and a negative driver.

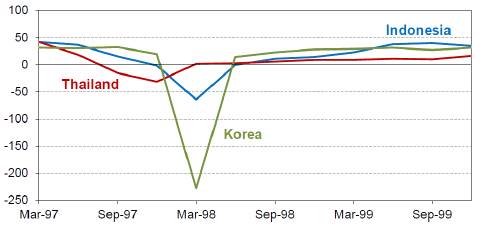

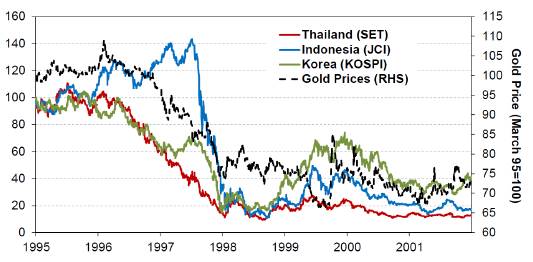

The impact of the Asian financial crisis is instructive. As the economies in the region fell into recession, the purchasing power of consumers in Southeast Asia declined commensurately. Thailand, Indonesia, and Korea all became net sellers of gold, albeit briefly (see Exhibit 1). In line with the drop in demand and the drop in the regional stock markets, gold prices fell 25% (see Exhibit 2).

Exhibit 1

Gold Demand During Asia Financial Crisis

Source: Bloomberg and World Gold Council

Exhibit 2

Gold Prices vs. Regional Stocks Market Indices (in US$

Source: Bloomberg and World Gold Council

While we do not necessarily believe that another Asia financial crisis is looming, the two biggest sources of gold demand – the economies of India and China – are coming under increasing pressure. This pressure may have already been dampening gold prices and may continue to do so going forward. According to the World Gold Council, consumer demand in India and China accounted for 37% of total gold demand in 2012.

India

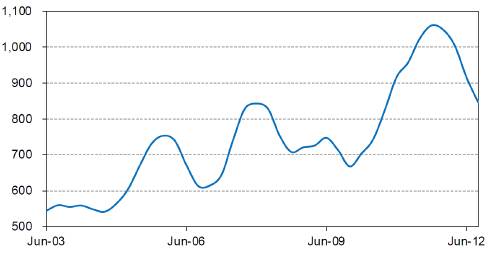

Since 2009, Indian gold demand has been somewhat unusual, with a burst of demand followed by a rapid deceleration (see Exhibit 3). The slowdown in India’s economic growth is at the crux of this change in gold demand.

Exhibit 3

Indian Consumer Gold Demand

Source: GFMS Ltd. (a subsidiary of Thomson Reuters)

India’s GDP growth has come down from the 8% to 10% rates of growth achieved between 2004 and 2010 to 4% to 5% growth over the more recent past, which is at a decade low. It’s not clear the infrastructure was in place to sustain growth at 8% to 10%. We had always believed that a slowdown was likely. Our expectations became reality when much-needed reforms were not passed by the government.

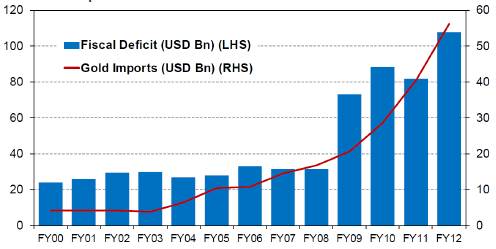

In line with the economic slowdown post 2008-09, the Indian government went on a spending spree to revive domestic consumption. The budget deficit increased from an average of 3.5% from FY05 to FY08 to an average of 5.7% from FY09 to FY12 (see Exhibit 4). Higher spending by the government led to higher inflation, which saw a rise from 2.3% in 2009 to over 9% in 2011. The rupee has continuously depreciated since 2008, having fallen by around 40% since then. Economic risks combined with high inflation made Indian consumers worry about the decline in purchasing power, causing them to buy gold. The buying of gold by Indian consumers and high imported inflation due to rupee depreciation led to a steep rise in the current account deficit, which in the quarter ending 2012 stood at 6.7% of GDP.

Exhibit 4

Budget Deficit and Gold Imports

Source: Reserve Bank of India, CEIC

Then, starting in late 2011, the continuation of these economic trends pushed gold demand in the other direction. A slowdown in economic growth limited the wealth gains of Indian consumers. Moreover, the depreciated rupee made gold that much less affordable in local currency terms.

This downward trend has been exacerbated by the government’s intervention in the gold market. Stung by concerns of the high current account deficit, the government is in effect shooting the messenger by targeting the gold market, as opposed to attacking the heart of the problem. Gold imports account for 3% of GDP per year. Without gold imports, the current account deficit would be 2% instead of an average of 5%. In its flawed response, the government raised custom duties on gold imports to 6% from 4% (according to Reuters). Effective February 15, 2013, parliament amended the PML Act, which heightened compliance standards for gold dealers. Even more worrisome, the finance minister has publicly discussed banning gold imports for one year. We do not believe that such a drastic step will be taken, but we also do not rule it out.

China

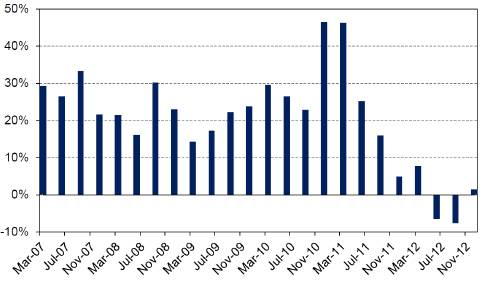

Similar to India, consumer gold demand in China cooled considerably in 2012, falling marginally on an absolute basis. This was in stark contrast to 2011 and 2010 when gold demand grew 22% and 32%, respectively (see Exhibit 5).

Exhibit 5

YoY % Chang

e in Quarterly Gold Demang

Source: GFMS Ltd. (a subsidiary of Thomson Reuters)

We believe that the strong demand in 2010 and 2011 was not so much the beginning of a higher sustained rate of growth, but a series of one-off events. The 2009 stimulus that led to the booming physical economy brought enormous “grey income” demand in 2011. But, the reshuffling of both central and local government officials introduced greater political uncertainty. Similar to the previous political cycle, this heightened gold demand.

More troublesome, as Edward Chancellor and Mike Monnelly point out, China’s credit system and economy are vulnerable. From their recent GMO white paper2 on China:

“China today seems to be in a similar predicament to several of the developed economies prior to 2008. Too much credit has been created too quickly. Too much money has been poured into investments that are unlikely to generate sufficient cash flows to pay off the debt. Last year, for instance, new credit extended to the non-financial sector amounted to RMB 15.5 trillion. That’s equivalent to 33% of 2011 GDP … The latest surge of credit follows the great tsunami of 2009, when China’s non-financial credit expanded by the equivalent of 45% of the previous year’s GDP. Since that date, China’s economy has become a credit junkie, requiring increasing amounts of debt to generate the same unit of growth. Between 2007 and 2012, the ratio of credit to GDP climbed to more than 190%, an increase of 60 percentage points. China’s recent expansion of credit relative to GDP is considerably larger than the credit booms experienced by either Japan in the late 1980s or the United States in the years before the Lehman bust.”

China’s gold demand is very sensitive to changes in economic conditions. In 2012, China retail sales alone accounted for 17.6% of global gold demand. Of this, roughly two-thirds came in the form of jewelry. If China gold demand were to slow, the impact on gold prices would likely be significant.

Conclusion

The concept of gold as a general insurance policy against systemic risks is dangerous, especially today. Gold prices are driven both by global monetary policy and emerging markets consumers. Emerging markets have been a significant positive force on gold prices for such a long time that it’s easy to forget that their impact on gold can very well go in both directions. Gold prices not only have extensive exposure to China and India, but their exposure to these countries is pro-cyclical by nature. Given both the cyclical and structural challenges the Chinese and Indian economies are facing, we believe the risks to gold prices today are particularly high.

The authors would like to thank Alvaro Pascual and Uday Tharar for their assistance in the preparation of this paper.

1 Amit Bhartia and Matt Seto, “Emerging Consumers Drive Gold Prices: Who Knew?” January 2012. 2 Edward Chancellor and Mike Monnelly, “Feeding the Dragon: Why China’s Credit System Looks Vulnerable,” January 2013.