"If the Fed tries to keep rates at or near the levels they are currently, it will signal that after so many years of policy accommodation, the U.S. economy is still too fragile to absorb even marginal rate hikes. Such a response would be tantamount to what we – and many others – have been saying for a long time: that the interest rate emperor has no clothes."

Tad Rivelle

TCW, January 15, 2016

Way back when many actually believed that an elite corps of technocrats could run an economy better than could a de-centralized market, the highest ranks of the Soviet planning bureaus grappled with solving that nation’s post-war housing crisis. Trade-offs had to be considered: was it better to have the construction “brigades” build the largest number of units possible, even if the units were cramped and shabby or should fewer but better apartments be the goal? These questions were debated loud and long at the central planning bureaus, but to what end? In the West, these questions were – and are – decided by consumers voting with their dollars. The West’s model managed to deliver the homes people wanted and could afford, without need of a housing “czar.” That is what markets do: they discover how resources should be priced and allocated without being instructed by officialdom.

The many and varied attempts to supplant market based pricing mechanisms with technocratic ones have had a disappointing history. Notwithstanding, the czars and czarinas at the Fed have given it the ol’ college try. The Fed has studied, analyzed, and debated where policy rates should be and for the entirety of this cycle up until one month ago concluded that the only “correct” answer was “zero.” Yet how is it that their “data driven” framework has always given the same result, even as the data has evolved remarkably over this cycle? As you think about it some more, might you also wonder whether the entire predicate of Fed based rate setting is a conceit of sorts?

The Fed has maintained that it knows what it is doing on policy rates and has clear objectives that it is attempting to achieve: higher growth, less labor slack, 2% inflation, and financial stability. But is there ever a single correct policy rate that achieves all of these objectives simultaneously? Might there be one rate that maintains sanity in the financial markets, another that guides inflation back to 2%, and a third that extinguishes the most slack from the labor markets? In short, the Fed has assumed that it understands the trade-offs between its various policy objectives and, consequently, should be empowered to steer the economy towards its fulfillment. Yet neither history nor an empirical reading of this cycle should be giving them – or us – much comfort. Growth targets have been sequentially missed, inflation has stubbornly held to levels that are “too low,” and financial stability…well, we’ll have more to say on that later.

In point of fact, the Fed has been trying to thread the eye of a needle with its policies and instead has tied a Gordian knot. The jobs market has been strong and with narrow measures of unemployment now at 5%, the case for raising rates further would seem to be clear. But then we must consider lowflation which argues against a rate rise. So too would the global collapse in commodity prices and the strength of the dollar. On the other hand, leverage has been building in the corporate sector and asset prices have, until recently, leaped while GDP has crawled, meaning maybe higher rates are essential to curtail speculative excesses. So riddle me this: should the Fed raise rates further in 2016?

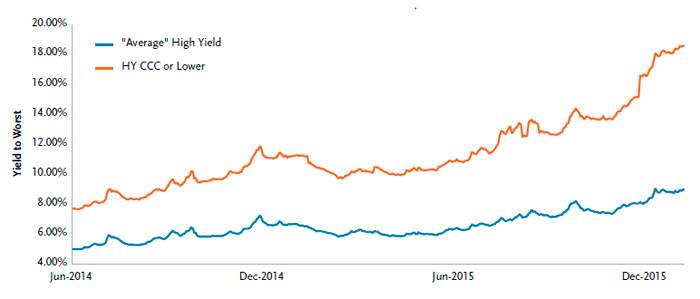

The answer is actually simple: the Fed doesn’t know and neither does anyone else. After seven years of having systematically suppressed rates and volatility, the technocrats are confronted with the reality that they are trying to answer questions that lack an objective response and should have been left to the market to decide. For instance, when gauging slack in the labor markets, how much significance was the Fed to accord labor force participation rates vs. unemployment rates vs. metrics on wage growth? In point of fact, the Fed has placed itself in the same untenable position that central planners everywhere sooner or later end up. By not deferring to the natural self-correcting influences of the capital markets, the Fed has most certainly committed a serious rate policy error. Their dilemma has now become obvious to all but the most sincere Fed apologists. Since 2014, commodity prices and EM currencies have collapsed, junk bond yields have soared, and disinflation/deflation is as entrenched as ever. Should the Fed now – belatedly – decide to raise rates in 2016 by the four steps that they say they will, we will almost certainly have a much flatter and perhaps partially inverted yield curve. If the Fed does move in this direction, a recession becomes a base case forecast. If the Fed tries to keep rates at or near the levels they are currently, it will signal that after so many years of policy accommodation, the U.S. economy is still too fragile to absorb even marginal rate hikes. Such a response would be tantamount to what we – and many others – have been saying for a long time: that the interest rate emperor has no clothes.

Yet, if rates cannot be normalized, then tautologically the cycle must end with policy rates still within spitting distance of zero. This reality counsels for a modest extension out of money markets into the front-end of the Treasury market. Meanwhile, vigilance is called for with “risky” assets: assets that are potentially “breakable” (non- mean reverting) need to be generally avoided until they actually “break”; “bendable” assets – those that do ultimately mean revert – can be added, albeit in a most disciplined manner.

In our mind, this turn of events has been foreseeable as monetary policy is a limited tool. Even as the Fed declared that nominal rates should not rise, its policies were enabling excesses in investment in the commodity complex that ultimately unleashed deflationary forces. As such, the market, in a roundabout way, “vetoed” low policy rates by, in effect, raising real rates as prices for commodities fell. Spreads on corporate, high yield, and emerging market debt have widened, in many cases, by extreme amounts. Again, the market has judged the real rate in these sectors as too low and has “sought” to raise them. So, in the end who was really in charge of interest rates?