“Evidently, bonds got tired of being called boring and decided to grab some headlines."

Fisher Investments Editorial Staff

Fisher Investments, 3 October 2023

On the latest volatility.

Evidently, bonds got tired of being called boring and decided to grab some headlines. Wednesday’s market coverage globally zeroed in on spiking long rates, portraying this week’s surge as a slow-motion global bond market crash gathering pace. Some tied it to yesterday’s House speaker vote, alleging uncertainty over GOP leadership—and what it means when a government shutdown is back on the table next month—rippled globally. Others see a global bond supply glut, while still others see higher long rates as a sign of ever-tightening financial conditions globally, drawing parallels with 1987. In our view, these theories have two big things in common: reading too much into short-term volatility and extrapolating present conditions forward. We think it is a mistake when people do this with stocks’ temporary wiggles, and we think it is an error now with bond yields.

Yes, yields are up. The 10-year US Treasury yield closed at 4.81% Tuesday, jumping 23 basis points (0.23 percentage point) from Friday.[i] It is down a few basis points (bps) today, as we write, but as widely reported, rates are still near a 16-year high. Yet some perspective is also in order, as we have seen some coverage use some funny math to exaggerate the magnitude of yields’ move this year. One article described the past six months as a 50% increase in US borrowing costs, which commits the classic sin of reporting a percent of a percent—a surefire way to artificially inflate a move.

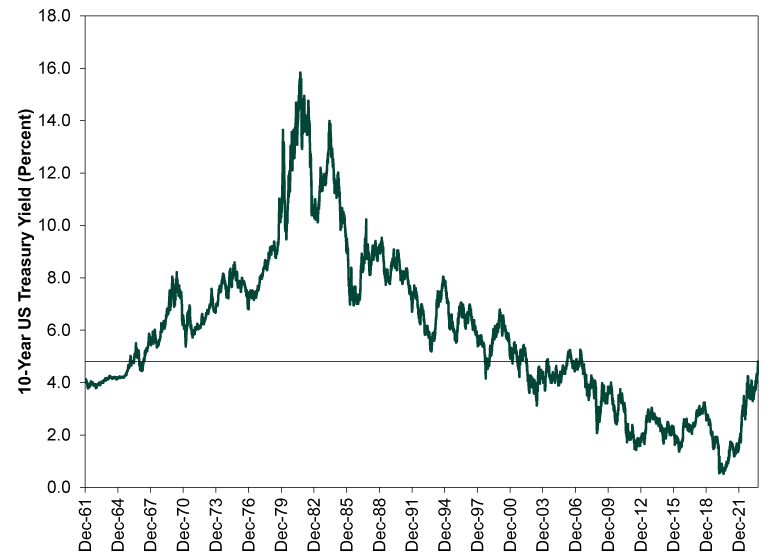

What it actually means is that the 10-year US Treasury yield rose from 3.30% on April 6 to 4.81% on October 3.[ii] That is an increase of 1.51 percentage points. Yes, it is nearly one and a half times that early-April reading, but a six-month increase of 1.51 percentage points isn’t unprecedented—it has just been a while. The most recent instance was in late-1993 and early to mid-1994.[iii] No financial crisis then. There was a crisis in autumn 1987, but yields’ rise then was much higher, surpassing 2.25 percentage points in six months.[iv] Yet yields moved about that much over rolling 6-month periods at various points in 1983 and early to mid-1984 without triggering a financial earthquake. Then too, in all of these instances, yields were rising off a much higher base. As Exhibit 1 shows, yields today are on par with the mid-2000s and well below the vast majority of the 1990s. These were hardly times of crisis or draconian austerity. (They were also quite nice for stocks.)

Exhibit 1: Yields’ Latest Rise in Historical Perspective

Source: FactSet, as of 10/4/2023. 10-year US Treasury Yield (Constant Maturity), 12/31/1961 – 10/3/2023.

That everyone is hyping the 10-year’s 16-year high and UK yields’ 25-year high (and other associated milestones) says more about how low yields have been this century than anything else, in our view. It seems like recency bias at work: People anchor to what just happened, rendering anything outside of that a shock even if it was the norm over the entire history. A measured view of history is usually a good antidote.

Another thing you will see in the chart: Bonds don’t move in straight lines. They wiggle. Their expected short-term volatility may be milder than stocks’, but bonds have their moments—their fair share of sharp moves that don’t last. We think this is the case today, and everything comes into focus—including why sentiment is so bad now—when you remember bond markets (like all similarly liquid assets) are forward-looking.

Today, the main source of fear seems to be that bond yields aren’t behaving as one would expect during periods of easing inflation. All else equal, bond yields reflect inflation expectations over the bond’s maturity, with higher inflation usually bringing higher yields to compensate for the bond principal’s eroded purchasing power. Falling inflation, at least in theory, brings falling yields. For the past half year, however, we have had falling inflation and rising yields. What gives? Simply, we think bonds pre-priced inflation improvement late last year and earlier this year. Markets saw the signs of it in the emerging data, anticipated further improvement, reflected that in prices, and then moved on. The inflation data—and inflation’s leading indicators—were just too widely known for there to be much (if any) positive surprise power left by the springtime. It got pre-priced.

Meanwhile, with economic fundamentals holding up much better than anyone expected, there was little to no reason for recession risk to pull long yields lower. Improving economic conditions also pointed to a deeply inverted yield curve that wanted to steepen, which would either mean falling short rates or rising long rates. Continued Fed hikes precluded the former for the time being, making it likelier than not that long rates would rise somewhat as this year wore on. In our view, this probably explains a lot of long rates’ slow rise since the spring.

But the magnitude of the recent move seems exaggerated by sentiment, in our view. Fundamentals haven’t changed, broadly. Yes, there is a lot of talk about rising bond supply, but this is a well-known factor. Investors have chewed over government bond issuance plans in the US, UK and rest of the developed world for months, and the latest auctions confirm the market is having little trouble absorbing it. The Fed and Bank of England’s balance sheet reduction plans are also well-telegraphed. There are whispers about reduced international demand for US Treasurys due to the dollar’s strength, but the limited data available don’t support this. In July, the latest report available, foreign holdings of US debt hit $7.65 trillion, close to the all-time high set in December 2021 and up over half a trillion dollars since October 2022.[v]

Absent major fundamental supply and demand shifts, there is a lot of talk. US House Speaker talk is one example, with headlines preoccupied over Kevin McCarthy’s ouster and the potential for a protracted replacement contest to interfere with budget negotiations and make a government shutdown likelier. But House gridlock isn’t new, and shutdowns have next to nothing to do with Uncle Sam’s creditworthiness, no matter what credit-raters like Moody’s claim. They also haven’t historically caused bear markets or recessions, as we showed last week. So yields’ jump seems like a classic overreaction.

Across the pond, a handful of UK city councils have issued Section 114 notices—widely reported as bankruptcy notices—spurring fears that the Treasury will have to bail out regional governments. But this is wide of the mark. One, per the House of Commons, “UK local authorities cannot go bankrupt,” and the Section 114 notices are simply formal notices that the council’s income will fall short of the next year’s projected expenses. The typical solution is spending cuts. Occasionally, councils will seek government permission to sell assets to meet the shortfall, or the central government will “intervene in how council services are run,” which generally amounts to cutting services. Outside a handful of small grants to support essential social services, central government funds aren’t involved.[vi] So the image of the UK Treasury borrowing bigtime to bail out city councils and creating a sovereign debt crisis seems far-fetched.

Bond market volatility—like stock market volatility—usually ends as quickly as it begins. The sharp moves can be painful, but staying cool is generally the wisest move, and we think it is wise today. It might be unrealistic to expect yields to get back to their springtime lows, given the fundamental reasons for yields to have drifted higher over the summer, but they don’t seem likely to keep soaring from here—and bonds should keep playing an important role for investors who need lower expected volatility than stocks alone would generate.

[i] Source: FactSet, as of 10/4/2023.

[ii] Ibid.

[iii] Ibid.

[iv] Ibid.

[v] Source: US Treasury, as of 10/4/2023.

[vi] “What Happens If a Council Goes Bankrupt?” Mark Sandford, House of Commons Library, 9/13/2023.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.